Because Croatia’s diaspora population is so vast, it is important for us to participate in the democratic processes regarding governance and representation in our homeland. The Croatian parliamentary system has especially addressed the importance of diaspora recognition and representation by way of the eleventh electoral district – to which three representatives are elected by and on behalf of Croatians living outside of Croatia.

A pertinent issue with diaspora voting however, is that voter turnout is often much less than it could and should be. Often times this is a result of no polling stations near Croatian communities abroad, but in some cases, there is also a sentiment that diaspora votes are negligible in the real outcome of the election.

To diminish this sentiment and to provide an insight into the political potential of the eleventh electoral district of Croatia parliament, Crodiaspora will be holding a public webinar debate with the candidates running to represent the diaspora. This includes Zdravka Bušić, running with Hrvatska Demokratska Zajednica (HDZ), Željko Glasnović, who is running for re-election as an Independent member of parliament in support of Miroslav Škoro’s Domovinski Pokret, Ruža Studer, running with Moja Voljena Hrvatska (MVH), and Slaven Raguž, running with the Bridge of Independent Lists (MOST). The debate will be live-streamed on Crodiaspora’s Facebook page at 7:30 P.M Croatian time.

In this debate, the aforementioned candidates will speak about their platforms and ideas for addressing any and all difficulties and concerns of diaspora communities around the world. Further, participation among viewers is encouraged and any questions for the candidates can be emailed to croatia@crodiaspora.com to ensure that viewers and potential voters can be directly informed of how their specific issues will be handled by each prospective representative.

It’s very important for the Croatian diaspora to understand each of their potential representatives and to understand what they can get out of each candidate’s platform to better their lives and their perspectives on the Croatian presence outside of Croatia. Diaspora communities continue to strive to grow and expand their connections with the homeland through social and business pathways, and these are some of the things they should seek experienced and apt representation for in the domestic Croatian democratic process.

Crodiaspora iduću nedjelju (28. lipnja) organizira sučeljavanje kandidata 11. izborne jedinice koji se natječu za mjesto u Hrvatskom saboru.

Sučeljavanje će biti održano preko online platforme Zoom. Na njemu će sudjelovati Zdravka Bušić ispred liste HDZ-a, Slaven Raguž ispred liste MOST-a, Ruža Studer ispred Stranke Moja voljena Hrvatska i Željko Glasnović ispred svoje neovisne liste.

Crodiaspora je udruga mladih Hrvata koji su rođeni izvan Republike Hrvatske, a sada djeluju u Republici Hrvatskoj.

As is well known among our Croatian diaspora communities, our base is large, vast, and powerful. Croatian diaspora has a clear and distinct presence in many established nations like the United States, Canada, Australia, Chile, Argentina, and of course throughout the rest of Europe. Although the estimates are rough, it has been recorded that there are over 2 million Croatians living outside of Croatia. This amount, considering that Croatia’s internal population is only just over 4 million is simply extraordinary. With such a global reach, the diaspora communities really hold a lot of hidden potential and influence with regards to their homeland.

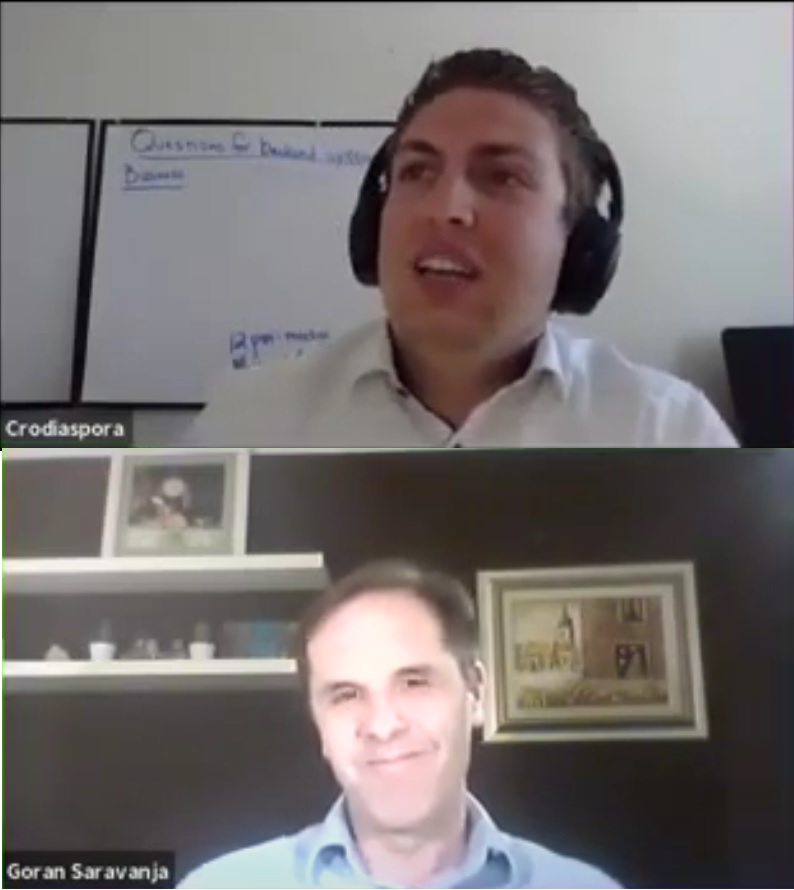

The positive impacts of Croatian diaspora can be highlighted through some success stories of individuals who have returned to Croatia from the diaspora and have made real change in the domestic spheres of politics, economics, and society. One such example can be shown through Goran Šaravanja’s detailed career in Croatian commerce as a returnee who was born and raised in Australia.

Article written by Peter Bury, Editor at Crodiaspora and Politicorp

Goran began his career in Australia at the New South Wales Treasury, which is a government department responsible for financial reporting, advising, and policy development. Shifting focus to Croatia, he worked in the Ministry of Finance, on macroeconomic forecasting and public debt management. In the private sector since 2001, Goran first worked as a regional Senior Economist at the Zagreb subsidiary of Austrian bank Creditanstalt Investment Bank, then moved on to work as Chief Economist at Croatia’s largest bank, Zagrebačka Banka as well as serving on UniCredit’s economic analysis team for four years. Next, from 2012-2017, Goran was the first ever Chief Economist at INA, in the oil and gas industry, and for his final two years there he also served as the head of Strategy Development. Most recently, Goran has founded a private consulting firm, IMELUM, which acts as an independent source for financial and business advising in South East Europe.

In a public webinar with Crodiaspora’s Mate Pavković, Goran shared some of his vast insights on working in Croatia, the process of returning to the homeland from the diaspora, and some of the future prospects for Croatia.

In discussing Croatia’s accession to the European Union and their fit and recent adaptations to the European framework, Goran outlines that although Croatia is a clear net recipient in the EU, he acknowledges that since joining the union, Croatia’s exports have surged and risk has diminished as a result of new direct and consistent access to a major consumer market in Europe. More recently, Croatia has garnered financial attention through hikes in their credit rating, which now stands as an investment-grade rating by multiple reputable rating agencies.

In terms of Croatia’s political atmosphere, Goran highlighted one major event that re-solidified the nation’s path to a stable democracy, and that was the short-lived government of Tihomir Orešković. Democracies have built in mechanisms like early elections, which Orešković faced, that prove democratic resiliency and flexibility in times of struggle, disagreement, and political deadlock. In this specific case, early elections did the work and maneuvered the nation to another government where agreements could be made to facilitate policy introduction.

Now, one of things that so many people in our diaspora wonder about is the business environment and potential in Croatia. Having substantial experience in that field, Goran talks about his interactions and conversations with foreign investors he met with mostly during his time with Zagrebačka Banka. He explains that their concerns with the Croatian business atmosphere is that there is an evident lack of ambition and lack of real expansionary effort among domestic businesses. He goes on to say that generally, Croatian business owners like to make their money, live a comfortable life, and that’s that – but what foreign investors are looking for and what Croatia is lacking are companies with real ideas and passion driving their growth, and ambition to really take the operations to the next level.

This is where diaspora can really play a transformative role in Croatia’s domestic growth and development. The simple fact is that we have grown up in nations with a different mindset when it comes to business; we have been exposed to more opportunities, and with them we get a greater degree of natural ambition. With these externally sourced assets, the Croatian diaspora has the potential to come back and act as an economic, political, and social driver for Croatian prosperity now and in the future.

Tasked with a diminishing population, as seen through our diaspora, attracting young people to come and live and work in Croatia must be one of the nation’s top priorities. Goran mentions that the issue with this is that emigration is not a Croatia-specific problem but rather one for all of Eastern Europe, and in any case, the major factor for attracting new professionals is all around stability, and that is something that must simply be fostered over several years.

One thing though that has been a central topic regarding Croatia in the European Union is their anticipated entrance to the Eurozone and adopting the euro as their main currency. The euro has the potential to be very good for Croatian commerce and trade as it will reduce transaction costs which are brought upon through currency exchange, reduce economic uncertainty, and provide an increased degree of financial transparency. With these economic stabilizers in place, Croatia will undoubtedly have an enhanced platform with which to advertise their eagerness to welcome new professionals and their ideas into our increasingly stable and reliable nation.

Further, with an increased Croatian participation in the European Union by way of joining the Eurozone, our accession to the Schengen Area nears. The Schengen Area is another facet of European connectedness of free movement by way of abolished border stops and customs checks. Needless to say, when Croatia joins the Schengen area, it will experience substantial boosts in overall movement of goods and labour as well as an influx in an already thriving tourism industry.

However helpful these additional EU mechanisms may be, Croatia still has outlying gaps in its own domestic economy. Namely, Croatia is not an economically diverse nation. With its GDP relying heavily on the service sector, industry and agriculture should be seen as opportunities where Croatians can take initiative and create a niche for themselves to carve out the framework for more domestic businesses. With energy giants INA and HEP dominating the high end of Croatian business, there is so much opportunity for ambitious professionals to build new industries and diversify the national economy into one where no one industry has to prop up the entire nation.

The fact still stands that there is such an abundant Croatian population outside of Croatia with such driving passion and ambition for growth and innovation and it would be a shame not to bring back some of that passion to the homeland to support growth and industrial advancements. From agriculture to computer technology, Croatia is a niche market with expanding economic potential by way of the European Union, and it can be a fantastic platform for small businesses to expand and thrive as opposed to being shut out of more established and rigid markets elsewhere.

Goran definitely has some excellent insights on the inner workings of Croatia’s economic system and financial sphere and his expertise is always recommended for anyone looking to invest or get involved in Croatian business, or any business operations in South East Europe for that matter.

For this result let’s also thank those who added pressure to the situation!

Thank you:

Garnett Genuis, Shadow Minister for Multiculturalism and Member of Parliament for Sherwood Park–Fort Saskatchewan

Garnett Genuis

Kenny Chiu, Member of Parliament for Steveston—Richmond East

Kenny Chiu

Tamara Jansen MP, Member of Parliament for Cloverdale—Langley City

Tamara Jansen

Nelly Shin, Member of Parliament for Port Moody—Coquitlam.

Nelly Shin

Marc Dalton, Member of Parliament for Pitt Meadows- Maple Ridge.

Marc Dalton Statement in Parliament

Bob Bratina, Member of Parliament for Hamilton East-Stoney creek.

Bob Bratina

They publically stood up for our right to vote and ultimately the government caved! And thank you all the Croatians out there who wrote to their MPs. Without you this result wouldn’t have happened. Democracy prevails!

Predsjednik Republike Hrvatske je 20. svibnja 2020. donio Odluku o raspisivanju izbora za zastupnike u Hrvatski sabor, koja je stupila na snagu 2. lipnja 2020.

Izbori u Generalnom konzulatu Republike Hrvatske u Mississaugi održat će se u subotu i nedjelju 4. i 5. srpnja 2020. godine od 07.00 do 19.00 sati

Generalni konzulat Republike Hrvatske u Mississaugi obavještava sve punoljetne hrvatske državljane koji borave na području provincija Ontario (osim Ottawe), Manitoba, Saskatchewan i Northwest Territories, a žele glasovati u GK RH Mississauga, o početku registracije za glasovanje u GK RH Mississauga.

Birači kojima je izdana hrvatska e-osobna iskaznica s adresom prebivališta izvan RH bit će registrirani po službenoj dužnosti prema adresi u osobnoj iskaznici, a ukoliko žele glasovati na području drugog diplomatsko-konzularnog predstavništva ili u Hrvatskoj moraju podnijeti zahtjev za promjenu mjesta registracije.

Za glasovanje u Mississaugi birači se mogu registrirati u Generalnom konzulatu RH u Mississaugi najkasnije do srijede 24. lipnja 2020. u 24:00 sata. U istom roku birači mogu odustati ili promijeniti svoj zahtjev za registraciju.

Svi birači mogu zaključno do srijede, 24. lipnja 2020. provjeriti svoj upis u registar birača na web stranici Ministarstva uprave RH https://biraci.gov.hr/RegistarBiraca/, u uredima državne uprave u RH, u diplomatskim misijama i konzularnim uredima RH i putem online sustava e-Građani te zatražiti izmjene eventualnih pogrešnih podataka.

Zahtjev za prethodnu i aktivnu registraciju birača podnosi se (osobno, poštom ili putem e-maila skenirano) Generalnom konzulatu u Mississaugi. Zahtjevu je potrebno priložiti presliku hrvatske putovnice ili osobne iskaznice, odnosno domovnice i kanadske putovnice ili vozačke dozvole.

The period before an election is a time to reflect on all that we have accomplished as a nation, while at the same time deciding the political discourse to honour those accomplishments, and to continue the legacy of our forefathers. As we reflect on what our country has accomplished, we cannot forget those who fought for those rights and advocated for the recognition of our country. This group of Croatians adopted a new country and continue to contribute to their new home, while at the same time give to their Motherland. Croatia is fortunate to have so many people that give their unconditional love despite their needs, their ideas, their knowledge, and their capabilities often being unrecognized.

The diaspora is Croatia’s unsung hero. Their legacy built our homeland. Unfortunately, for this upcoming election their rights are being diminished due to the Corona Virus. However, it is not the Corona virus that ultimately failed them, but instead, we failed to digitize and implement modern ways to vote.

Canada is a perfect example of the necessity of Electronic and Mail-in voting.

There is a geographic barrier as many Croatians in Western Canada are not within 4,000 Kilometers of a polling station.

This leads to an economic barrier as flying within Canada can be as expensive as flying to Europe.

Out of the over 7,000 registered voters, barely 10% of them vote in Croatian elections.

In the short term these issues cannot be fixed, in the long term, there is hope. However, one thing is for sure: our fight as diaspora is not over.

If you are a Croatian Canadian, you have the right to contact your local MPs. The power of the pen (or keyboard) is more powerful than any sword. People can assemble to protest in the hundred of thousands, but why can we not vote due to social distancing? Is there no way that we can compromise and find an appropriate way to cast our vote? These questions need to be posed and you need to demand your democratic right as a citizen of both countries.

Contact your local MP and demand your fundamental right as a Croatian Citizen to vote. Croatian Canadians and all Croatians in the diaspora are paramount to Croatia’s democracy. To find out who your local MP is, click here.

Some other people you should include in your emails are:

Bob Bratina, MP Hamilton East- Stoney Creek (Croatian Canadian)

Razdoblje prije izbora vrijeme je za razmišljanje o svemu što smo postigli kao nacija, a istodobno odlučivanje političkog diskursa u čast tih postignuća i nastavak nasljeđa naših predaka. Kao što razmišljamo o onome što je naša država postigla, ne možemo zaboraviti ko se borio za ta prava i zalagao se za priznanje naše zemlje. Ova je skupina ljudi usvojila novu zemlju i doprinijela je njoj, a istodobno daje sve za svoju Domovinu. Hrvatska je posebna po tome što ima tijelo vlastitih ljudi koji daju bezuvjetnu ljubav, unatoč tome što često zanemaruju njihove potrebe, svoje ideje, znanje, sposobnosti i nadasve svoj doprinos u osnivanju zemlje.

Dijaspora je hrvatski nestali heroj. Njihova je ostavština naša domovina. Nažalost, ovim izborima njihova prava se umanjuju zbog virusa Corone, ali u konačnici i zato što nismo uspjeli izračunati i primijeniti moderne načine glasovanja.

Kanada je savršen primjer potrebe za glasovanjem putem elektroničke pošte i pošte.

• Postoji geografska barijera jer mnogi Hrvati u zapadnoj Kanadi nisu na 4.000 kilometara od biračkog mjesta.

• To dovodi do ekonomske prepreke, jer letovanje unutar Kanade može biti skupo kao i let u Europu.

• Od preko 7000 upisanih birača, jedva 10% njih glasa na hrvatskim izborima.

To se u kratkom roku ne može popraviti, dugoročno postoji nada, ali jedno je sigurno: naša borba kao dijaspora nije gotova.

Ako ste hrvatski Kanađanin, možete se obratiti lokalnim zastupnicima. Snaga olovke (ili tipkovnice) je snažnija od bilo kojeg mača. Ljudi se mogu okupiti na prosvjedu pred stotinama tisuća, ali mi ne možemo glasati zbog socijalne distancije? Ne postoji li način da postignemo kompromis i pronađemo prikladan način da dodijelimo svoj glas? ta pitanja moraju biti postavljena i trebate zahtijevati svoje demokratsko pravo kao građanin obje zemlje.

Obratite se svom lokalnom zastupniku i zatražite svoje osnovno pravo kao hrvatskog državljanina. Hrvatski Kanađani i svi Hrvati u dijaspori najvažniji su za hrvatsku demokraciju. Da biste saznali tko je vaš lokalni zastupnik, kliknite ovdje.

Neki drugi ljudi koje biste trebali uključiti u svoje adrese e-pošte su:

Bob Bratina, saborski zastupnik Hamilton East- Stoney Creek (hrvatski kanadanin)

On Monday June 1st, Crodiaspora and the Center for the renewal of Culture (COK) held their third webinar with Tax expert Hrvoje Jelić and country Managing Partner at PwC Croatia, John Gašparac. They discussed and addressed the tax concerns of Croatians abroad who are contemplating business opportunities and returning to live in Croatia.

In addition to the summary, we have included additional resources to use when making business and personal tax decisions in Croatia. Although this webinar and article offers general information about the tax situation in Croatia, John expressed at the beginning of the webinar that unless your tax advisor knows everything about you, your finances and your income, it is hard to understand the nuances of the tax exemptions and benefits you may receive. If you would like to get in contact with Hrvoje, John or other business advisors at PwC Croatia who can get to know your financial situation better and advise you in Croatia, you can do so by clicking here.

Due to the abundance of information in this article, we have created anchors below to help you navigate to the topic(s) you are interested in. The topics discussed were:

We hope that this webinar and article will give you an idea of how the Croatian tax system works. Stay tuned as we have more informative and entertaining webinars planned for the near future.

CROATIAN TAX STRUCTURE

To watch Hrvoje explain the Croatian tax system click here.

Hrvoje began by complimenting the Croatian tax system and how there has been many amendments in the past 20 years and it is now more business friendly. Especially over the past 4 years, there have been many rounds of tax reforms that have been implemented on the first of January of every year.

The Croatian tax system can be broken down into 3 major tax revenue streams. VAT taxes and excess duties which amount to 50 billion HRK per annum and almost 50% of the state budget; Corporate income tax which collects somewhere around 8-8.5 billion HRK per annum; And personal income tax which amounts to 15 billion HRK per annum. These are the three main taxes in Croatia and are the most referred to when discussing tax reforms.

If you want more information about the tax structure in Croatia:

To watch Hrvoje explain Corporate and Personal income tax click here.

In Croatia by definition, all companies are corporate income taxpayers. Every company in Croatia is treated as if they were a ‘person’, since it has an OIB (personal identification number) and subject to tax. Hrvoje points out that how much a corporation pays in tax is not solely determined by their profit but also by their revenue. “[This] is a bit strange for some people because we apply two tax rates 12% or 18% for corporate income tax, but the lower tax rate is applied on income derived from revenue of less than 7.5 million HRK, which is around 1 million euros.”

So just to make that clear, if you are making 7.5 million HRK, if you are in that bracket, you are paying 12% tax, but once you get above that you are paying 18% on everything, right?”

Hrvoje then clarified by saying, “Yes. this is specific. It is not a tax bracket like the case of personal income tax. In personal income tax if you earn up to 360,000 HRK per annum you pay tax at 24% plus surtax, if any, depending on place of residence. On anything above that, meaning on the surplus pay, you will be paying 36%. It is not the case that you pay 360,000 HRK and you pay 36% on everything. These are not tax brackets but instead are progressive tax brackets.”

When an employer pays an income to an employee, what are the responsibilities of the payer? Are there items they pay for besides withholding their taxes?

“This is related to individuals, but in Croatia unlike the US for example, when you have a payer of income (Employer), then the payer and not the employee is obliged to calculate, report, withhold and pay tax on your behalf. This makes the system quite straight forward and rather simple and user-friendly for individuals who are the taxpayers. You have a taxpayer, but you also have someone that has to take care of the individual’s taxes which in this case is the employer.”

He then explained the responsibilities employers have to pay social security contributions for their employees, “We have 2 kinds of contributions. We have a contribution for health insurance which is normally the burden of the employer (it comes off of your gross salary) and we have pension contribution(s) which amounts to 20% and might be divided into 5% and 15% proportions depending on how you contribute (if you contribute to a public and private fund it is usually divided in the 5 and 15% proportions).” The only people that pay the full 20% to the public fund instead of the divided 5% and 15% are some people over the age of 50.

What happens if you work for a foreign company in Croatia? Who is responsible to pay your income?

“If you are employed with a company which is abroad and you are receiving income from abroad, then you do not have a domestic payer of income. This liability of calculating, reporting, withholding, and paying tax is transferred over to you. For example, if you receive a dividend from your Croatian payer, then the Croatian payer will be obliged to calculate and withhold tax and pay your net amount. [The payers of the dividend] are also responsible to report to the tax authority. But if you are receiving a dividend from abroad then you have to do it for yourself.”

If the employer needs to pay and report taxes on their employees’ income to the tax authority, do Croatian tax residents need to file a tax return?

Hrvoje began by outlining the reasons for the modern Croatian tax system and why Croatia switched from individual taxpayers reporting tax to employers reporting tax. “Filing (in Croatia), is much unlike the filing that happens in the US or in Canada. This is because the Croatian tax authority wanted to simplify the system because many years ago it was the rule that every person who earned any kind of income was obliged to file an annual tax return. The deadline was the end of February for the previous year. Then the tax authorities realized that many people were filing their annual tax returns and there was no tax to be paid. In addition, there was no tax to be refunded to them. Basically, people were paying throughout the year the exact amount of tax that they were obliged to pay on an annual basis.”

“Now we have the simplest possible system where there are different filings on a transaction basis. For example, if you receive a dividend, somebody reports the transaction depending on what I said earlier (depending on if it is a domestic or foreign dividend). This way the tax authorities in real time, i.e. within a delay of a month, can receive all the information about your income. Then they calculate the income for all of us once per annum after the year has expired. They will determine whether we need to pay something in addition. In that case they issue a tax resolution to us. We can also receive a refund which is then paid to your bank account.”

He concluded by highlighting that, “people who need to file annual tax returns are usually sole entrepreneurs and seamen.”

If you want to calculate tax, social security, and health contribution you can use the mojposao salary calculator by clicking here. For those who want to open a business and would like to find out about what incentives you are eligible for, you can Use the Ministry of Economy’s tax benefit calculator by clicking here.

DOUBLE TAXATION AGREEMENTS

To watch Hrvoje explain Double Taxation click here.

Many Croatians that live in Australia and the United States are concerned about double taxation and the potential barriers for feasible business transactions. They are also concerned about returning to Croatia and potentially being taxed twice on their income.

Double Tax treaties

“This is a very interesting topic, but it’s a bit complex. So, if you allow me, I would like to provide some general information so that our audience understands the principle of double taxation. I think most questions will already be answered through that. I would like to say that Croatia has a pretty good network of double tax treaties. We have now, I think, with 66-67 countries in the world including some exotic countries like Mauritius.”

He continued by addressing the absence of a double tax treaty between Croatia and Australia and Croatia and the United States. “That is true that we do not have a double tax treaty with Australia or the United States. I do not know why Australia, but I do know with the US there have been many attempts and initiatives. The problem lies on the American side because they have not been interested. The Americans would like to see something that we call in business, business case. They would like to see a certain volume of transactions between the United States and Croatia to even enter negotiations for the double tax treaty.”

Croatia has a double tax treaty with all other EU countries except Cyprus. Croatia also has double tax treaties with countries such as Canada, Russia, the United Kingdom, and the United Arab Emirates. To see a full list of countries you can click here.

How rare does double taxation occur and how can I avoid paying double tax when my country does not have a double tax treaty with Croatia?

“The principle of avoiding double taxation is much easier when you have a double tax treaty. Although, even if you do not have a treaty, such as the case of the US or Australia, it does not automatically mean that you, as a Croatian tax resident, would pay tax in two places at the same time. Double taxation is defined as paying tax on one individual’s same income in two different countries. So, in practice it very rarely occurs.”

Croatia follows a special principle to avoid double tax. If you are able to prove that you have paid tax on an income, whether it be a personal income, a dividend, or anything else that is taxable both in Croatia and in the foreign country taxing the item, then Croatia recognizes that you paid that tax and if the tax was less in the foreign country you pay the difference.

“Croatia applies a unilateral measure for avoidance of double taxation. These are basically measures where if you are able to prove to the Croatian tax authority that you paid some tax in the US, (lets assume that you received a dividend from a company in the US), and you have reported to the Croatian tax authority this tax is waived. For example, if you said that the US payer of the dividend withheld 20% tax, what the Croatian tax authorities will do next is say that in Croatia you will be liable to pay an effective tax rates of 14.16% on dividends from abroad. So, the Croatian tax authorities would say, on every $1,000 you would pay $141.60 in tax. But since you already paid $200 in the US which were withheld by the payer, we will just simply credit the Croatian tax against the American tax liability meaning I will not pay any further tax. So effectively, I only paid tax in the US, I report it in Croatia and my tax liability in Croatia is deemed to be covered by the US tax.”

What if the amount of tax paid in a foreign country on foreign income is less than what would be taxed in Croatia?

In this example, “if the tax came out to be less in the United States for that dividend and in Croatia it was higher, than you would pay the difference to the Croatian tax authority. If I only paid 10% tax in the USA, then I will need to pay an additional 4.16% on the gross amount in Croatia. But I will not pay tax in two different countries at the same time.”

“So, people need not to be worried about a situation in which they would really be double taxed, which means that they will pay tax on the same income in two different countries. Unless they are for any reason unable to prove that they really paid tax in another country or they cannot recall how much they paid in that other country.”

What is the purpose of a double tax treaty?

“When there is a double tax treaty then the situation is better for the taxpayer. The double tax treaty is an agreement between two separate states where they define that certain individuals or corporations are a resident of either of those two states. So, for the purpose of the application of a double tax treaty you will be defined as a tax resident of one of those two states only. Even though based on domestic regulations of both states you might be a tax resident of both of them.”

Hrvoje highlighted the details of Article 4, in the double taxation treaty which outlines the country of residence of the citizen affected by the treaty. “But to make it possible to apply the treaty, article 4 defines residency based on certain criteria. As an example, based on the treaty I am a Croatian tax resident; I receive income from let’s say Germany…. So typically the treaty would say: If Hrvoje is a Croatian tax resident and receives a dividend from a German corporation, and the German corporation pays this dividend to Hrvoje, then Germany is entitled to tax this particular income, lets say at 10%. In layman’s terms, the countries are agreeing on how much tax each country will take. In this example, my country of residence is theoretically entitled to tax my worldwide income because I am a Croatian tax resident including this dividend from Germany.”

He continued by explaining the two methods in which these treaties avoid double taxation. “There is the exemption method, which means my country would treat my German income as if there was no income, so they would just ignore it, or the credit method. Ex.‘So, you, Hrvoje, have paid 10% tax in Germany, you need to pay 14.60% in Croatia, you will only pay the difference because we will treat German tax like it was Croatian tax. For me as an individual, I will always pay a certain amount of tax but the two countries, in this case Germany and Croatia, will have agreed on how much tax each one of them will take.”

He concluded by addressing why it is in Croatia’s interest to have a double tax treaty with the United States. Croatia’s foreign tax principle where Croatia “unilaterally says, ‘OK, you pay tax in the US, we will not tax you at all’. This is not the case when you have a double tax treaty because for every type of income it is always stipulated which country needs to do what and who is entitled to what amount of tax.”

CROATIAN TAX RESIDENT

To watch Hrvoje explain what is a Croatian Tax Resident click here.

One of the ways that you can avoid paying tax in another country is to become a tax resident of another country. Hrvoje outlines the criteria to be a Croatian tax resident.“In Croatia, these rules have also developed over time and today we have a pretty good situation. Normally you would be a Croatian tax resident if you permanently live in Croatia which means you have a permanent home or a home at your disposal (renting) or you have a habitual abode. An example of a habitual abode is if you come to Croatia for 4 months or 6 months every year this means you have a habitual abode in Croatia… generally speaking, if you have a home available in Croatia, you might be able to consider yourself a Croatian tax resident.”

What if you have a Permanent residence somewhere outside of Croatia?

“If at the same time, you have a permanent home elsewhere, in a country where we apply a double tax treaty, then the rules from article 4 will be applied. There are criteria. If you have a permanent home in both countries, then you cannot determine what country you are a tax resident in. The next criteria are applied and the next are applied to determine your status but usually we come to a criterion called the ‘center of vital interest’. The center of vital interest applies to either where your family lives, (meaning your immediate family, your spouse your kids…), or where there are strong economic ties. Croatia introduced this criterion from the OECD convention on which all Croatian double tax treaties are based,” Hrvoje explains.

American citizens were in an ambiguous situation a few years ago: “Let’s say if a US citizen has a house in Croatia, and they spend 6 months a year here. Based on Croatian legislation at the time, they would be deemed Croatian tax residents. Today it is better since you can now say that you do have a home in Croatia, I spend 4-6 months there, but my center of vital interest is still in the US. This is because most of my assets are in the US, my income comes from the US, my children live in the US. You are then not a Croatian tax resident but an American one. Currently you do not need to report to the Croatian tax authorities and report your worldwide income. You will only need to report your Croatian sourced income if any.”

US CITIZENS

To watch Hrvoje explain the American tax situation click here.

The United States is an unusual case because taxation is not based on whether you are a tax resident rather, the Americans are taxed based on citizenship. If you are an American citizen abroad, then you are an American taxpayer. “According to the best of my knowledge, all EU countries tax their people based on their residency and not citizenship. It is irrelevant from the Croatian point of view in many cases, what citizenship you are holding and whether you are a Croatian citizen. From the Croatian point of view, for tax purposes, it matters whether you are a Croatian tax resident. But what if you are not a Croatian tax resident and you may have a Croatian sourced income? For example, you have a house here and you rent it out and you have rental income which is taxable. This is Croatian sourced income and Croatia is entitled to tax based on domestic laws.”

Hrvoje summarizes by saying that, “If you are a Croatian tax resident, you technically pay tax on all worldwide income. We say this but you report your income from anywhere in the world to the Croatian tax authorities. Whether you are obliged to pay taxes on that income depends on whether the income is even taxable in Croatia and whether you paid tax on your income abroad.”

What if I make a Croatian income, will I be taxed in the United States?

For this question we consulted the former associate counsel for the IRS who directed us to US tax Code 26 USC 911 which outlined the tax obligations and exemptions for US citizens living abroad. All US citizens who make above the minimum taxable amount need to file a tax return. The minimum taxable amount in 2019 was $12,200.

If you live in Croatia for a full tax year (i.e. January 1st- December 31st) without leaving the country, you are considered a bona fide US foreign resident. The IRS will need further information about your residency status in Croatia. You will need to fill out US form 2555, to be able to apply for a tax exempt amount of foreign income.

In 2005, the tax exempt amount was $80,000 and each year the amount has been adjusted for inflation. This amount is now $105,900 (either in US Currency or foreign currency equivalent). This means that you can work and live in Croatia, and are able to earn up to $105,900 in Croatia without it being taxed in the U.S.A. You will still have to file a tax return and declare this status every year while living abroad.

This status may be different for those with mixed incomes where the source of income is from the United States and Croatia. Be sure to seek proper tax guidance as every situation is different.

DIGITAL NOMADS

To watch what Hrvoje has to say about the tax situation for digital nomads click here.

A Canadian lady asks: if I have a home in Croatia but my income is from abroad, do I pay any sort of tax in Croatia?

“Firstly, I would encourage this lady to seek proper tax advice, as I would encourage everybody who has any business in Croatia or has any income which might be subject to Croatian tax. As John mentioned at the very beginning of this webinar, every situation is different. These are general situations and it can provide general ideas. In this case, there are tests, which need to be performed. Firstly, we need to determine if the lady is or is not a Croatian tax resident. If not, most probably not, then she might be liable to pay certain taxes in Croatia. But this depends on the type of income. If she is an employee of a US corporation for example, and she works in Croatia and she receives income while physically being in Croatia, she might be liable for Croatian tax. If this is the same case with Canada for example, where we have a double tax treaty, then certain different tools will apply.”

Hrvoje continues by saying, “If I remember correctly from article 15[in every double tax treaty] this is employment income. We would then need to do some more tests whether her salary is charged to a Croatian entity which here is not the case. In that case, she most probably would not pay any Croatian tax on that sort of income. If you don’t mind I would stop there because there are many details which need to be taken into account for that kind of situation, but generally speaking we may say that if you are not a Croatian tax resident based on those criteria that I explained a bit earlier, then in the majority of situations as a digital nomad you would most probably not enter into the position to pay Croatian tax. Although whenever you buy something, you are paying Croatian tax in the form of VAT.”

RETIRING IN CROATIA

To listen to what Hrvoje has to say about the tax situation for retirees receiving a foreign pension click here.

What happens if you come to Croatia to retire, cut your ties from your former country, to become only a Croatian tax resident? In other words, you want to pay taxes on your pension only in Croatia.

“This is a very good question and a very good example. Prior to answering I will just tell you something about the former situation which made Croatia extremely attractive for people in this same situation. I have had several cases of retired Swedes and Brits. They also were receiving dividends and/or capital gains and they moved to Croatia and purposefully became Croatian tax residents. They wanted to cut all their ties to their home countries since in Croatia there was literally no tax on foreign pensions. That point in time, Croatia did not tax dividends, capital gains, and foreign pensions.”

He then highlighted the turning point where the Croatian tax authorities started to tax pensions from abroad. “Also, during that time Croatia was negotiating their double tax treaty with Switzerland and there are a lot of diaspora that live in Switzerland. When these Croatians earned their pensions, they would come live in Croatia. When negotiating the double tax treaty, the Swiss authorities were reluctant to accept the usual clause about taxing people in the country of residence which in this case Croatia, is the only country entitled to tax Swiss pensions of Croatian tax residents.”

“Switzerland was hesitant because they said, ‘but then this income will not be taxed anywhere, because we are not allowed to tax it and Croatia is not taxing it.’ The point of the double tax treaty is not to tax the same income in two countries, but it also has a purpose to not to avoid tax all together. No one should have a situation in which you do not pay tax anywhere. The Croatian tax authorities insisted on having this clause and the Swiss finally accepted it. A few years after that, Croatia changed its laws and introduced tax on foreign pensions.”

One thing that is important to note is that cheques are not cashable in Croatia as John points out. If you do receive your pensions via cheque, John suggests to set up an automatic deposit every month or learn how to use your Mobile banking app so that you, or a loved one, can cash it via mobile device.

PROPERTY TAX

To hear the kinds of property taxes there are in Croatia click here.

Croatia is also attractive from this perspective. Property taxes do exist in Croatia, but the amount is very insignificant. “For example, you have property taxes on summer cottages, or summer apartments, you are paying a little bit more than 100 Euros per year. This is insignificant. There is also property tax on personal vehicles. Maybe 150 Euros per annum. It depends on some criteria like the square meters, the zoning and for cars the value, but it is very insignificant.”

He goes onto to add that the closest thing to property taxes on your first home in Croatia are monthly communal charges. “I am living in an apartment of around 120 square meters and I pay these communal charges that can be considered a tax. This ‘tax’ is around 150 HRK per month. Even though these property taxes do exist, they are very cheap.

INHERITANCE TAX

To hear Hrvoje talk about Inheritance Tax in Croatia click here.

This was partially answered in last weeks webinar about the Croatian legal system. If you are inheriting a property in Croatia from an immediate relative (parents, grandparents, brother, or sister) then you do not need to pay property tax. As Hrvoje says, “There is a wide group of exemptions [for the 5% inheritance tax].” Another exemption is when you transfer ownership or real estate and you pay the 3% tax for transfering ownership. If you paid this tax, then you are exempt from paying the inheritance tax. These rules apply for Croatian and non-Croatian citizens.

CONCLUSION

This was a complicated topic, and this was a generic overview of the Croatian tax system. The explanations expressed in this article are just general guidelines and Crodiaspora and COK encourage you to contact a tax advisor to assist you if you are unsure about your tax situation. There is no such thing as a simple tax question. There are always exceptions that may apply to your situation. We hope that this webinar and article has given you a taste of the Croatian tax system. Stay tuned as we have more informative and entertaining webinars planned for the near future.

Are you a Croatian abroad and are considering moving back to Croatia? Are you unsure of what taxes you have to pay on your income, pension, or on assets abroad? Are you an American and Croatian citizen and are confused by what double taxation entails?

John Gašparac, Country Managing Partner at PwC Croatia (Photo: PwC Croatia)

On Monday June 1st, 2020 Crodiaspora and COK will be hosting John Gašparac, Country Managing Partner at PwC Croatia, and Hrvoje Jelić, Partner leading tax & legal services at PwC Croatia as they answer your questions about taxation in Croatia. The webinar will be broadcasted live on Crodiaspora’s Facebook page here.

Hrvoje Jelić (Photo: PwC Croatia)

“As many people have offered to give Crodiaspora donations, we did not feel right at this time to accept them. This is why, along with our partner at PwC and ACAP, we have decided to make this webinar a fundraiser for the ACAP Earthquake relief fund to help rebuild hospitals in Zagreb. If you are able to do so, and find what we are doing at Crodiaspora helpful, we ask you to donate to this worthy cause. ACAP has raised over $40,000 and we would like to help them reach $50,000 by the end of the webinar on Monday,” Crodiaspora said.

You can send them your questions at croatia@crodiaspora.com and they will try to answer them all on Monday. Details on the poster below.

Are you a Croatian abroad and are considering moving back to Croatia? Are you unsure of what taxes you have to pay on your income, pension, or on assets abroad? Are you an American and Croatian citizen and are unsure of what double taxation entails?

Join us on Monday June 1st at 6:30 P.M Croatian time (UTC+2) for the third Crodiaspora- COK online academy webinar. We are excited to have John Gašparac, Country Managing Partner at PwC Croatia, and Hrvoje Jelić, Partner leading tax & legal services at PwC Croatia to discuss what you need to know about the Croatian tax system.

This webinar will be free but if you like what we are doing with Crodiaspora, we ask you to donate to the ACAP Earthquake fund for the reconstruction of hospitals in Zagreb. The Association of Croatian American Professionals launched this crowdfunding campaign to help those affected by the earthquake, especially those in hospitals that were damaged during the earthquake. If you are able to do so, we highly recommend to donate to this worthy cause. Find out more by clicking here.

Send us your questions at croatia@crodiaspora.com so that John and Hrvoje can prepare their tax advice. The webinar will be available on Crodiaspora’s Facebook Page.

By continuing to use the site, you agree to the use of cookies. more information

The cookie settings on this website are set to "allow cookies" to give you the best browsing experience possible. If you continue to use this website without changing your cookie settings or you click "Accept" below then you are consenting to this.